By Blair Lozier

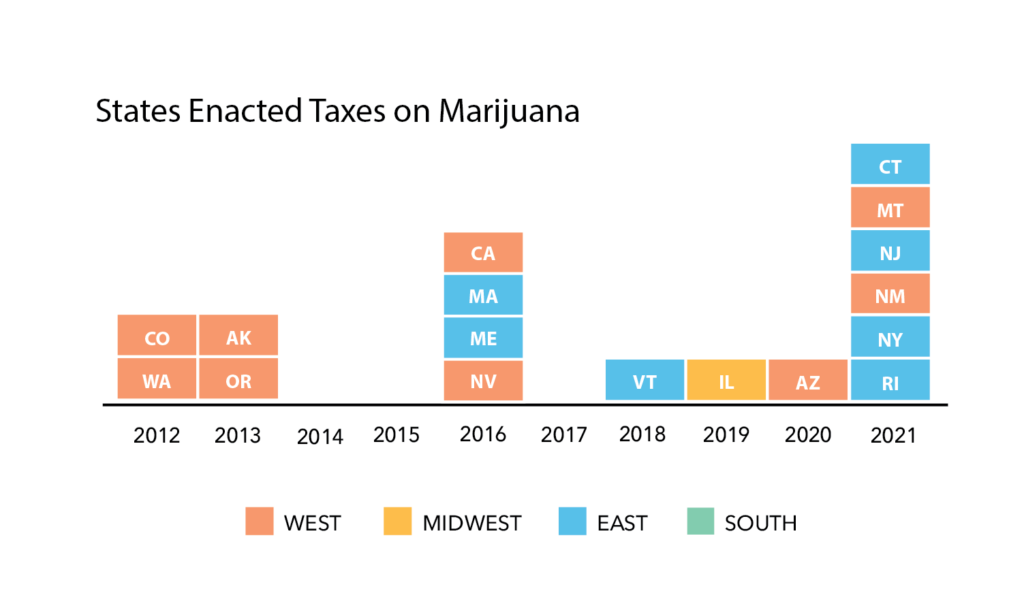

Recreational marijuana has been legalized in 19 states since 2012. Washington and Colorado were the first states to collect taxes on recreational marijuana. As of June 2022, 12 states have data available on taxes collected: Alaska, Arizona, California, Colorado, Illinois, Maine, Massachusetts, Michigan, Nevada, Oregon, Vermont and Washington. Seven states – Connecticut, Montana, New Jersey, New Mexico, New York, Rhode Island and Virginia – have legalized the recreational use of marijuana, but tax collection data is not yet publicly available.

As more states legalize recreational marijuana use, new tax collection methods have been developed. Six states legalized recreational marijuana in 2021, and each one uses a different tax structure to collect revenue on those transactions.

Below is a graph demonstrating the number of states by year that recreational use of marijuana was legalized.

Tax Collection Methods

There is no federal regulation on how states can collect marijuana taxes. States have commonly used three methods for collecting taxes.

1. Percentage-of-price

The consumer pays a tax on the total price of the purchase. The tax varies by state/local district and is set at a higher percentage than regular sales taxes.

2. Weight-based

The distributor is responsible for paying an initial tax based on the weight of the product within various categories of marijuana. Then, the retail distributor adds a tax to the closing price of the retail sale. Different types of marijuana and different parts of the marijuana plant can be taxed separately. For example, states can establish a tax on the flower of a marijuana plant that is different from the tax established on marijuana leaves.

3. Potency-based

The tax level is based on the amount of THC (Tetrahydrocannabinol) in the product being sold. Tax percentages vary across states.

State Approaches

The percentage of price is the most common method of taxing recreational marijuana sales (12 states). Maine is the only state that collects the tax through the weight-based method. Illinois is the only state to collect through just the potency-based method. Alaska, California and New Jersey collect taxes through weight-based and percentage-of-price. Connecticut and New York collect taxes through potency-based and percentage-of-price.

Local governments receive most of their revenues from taxes on property and sales. States often give discretion to localities and municipalities to determine their tax rates. Every state except Illinois, Maine and Michigan allows local or municipal governments to collect an additional tax on marijuana purchases.

Even if states implement a weight-based system, many allow localities to implement a percentage-of-price system enforced where the marijuana is purchased.

States dedicate revenue generated from marijuana sales toward various government programs. For example, Arizona uses a percentage-of-price based tax system and dedicates 33% of revenue to community college funding, 33% to law enforcement and fire departments, 24% for the cost of enforcing the new marijuana law and 10% for the Justice Reinvestment Fund. The Justice Reinvestment Fund was established in 2006 to identify opportunities for change and improvement in the criminal justice system.

Many states use the revenue generated from marijuana sales to fund socio-economic programs to support individuals with drug offenses, economic development and educational and community-based initiatives. Several states dedicate revenue generated from marijuana sales toward various government programs. Most states have multiple uses for the revenue generated from recreational marijuana. On the other hand, Colorado, Massachusetts, Rhode Island, Vermont and Washington dedicate all the funding generated from recreational marijuana retail sales to one specific purpose. Rhode Island and Washington allocate these funds to public health and health care systems. Colorado and Vermont support education programs. Massachusetts dedicates funds to public safety. All five states collect tax under the percentage-of-price tax system.

| State | Taxable Amount | Revenue Dedication |

| Alaska | Weight-based $50 per ounce for flowers $15 per ounce for stems and leaves $25 per ounce for immature flowers and buds $1 per clone Percentage-of-price Localities can levy a percentage of the price | 50% for programs to reduce repeat criminal offenses 25% for drug education and treatment programs 25% for the state’s general fund |

| Arizona | Percentage-of-price 16% for fall retail purchase 5.6% state general sales tax Localities can generate a local sales tax. | 33% for community colleges funding 33% for law enforcement and fire departments 24% for the cost of enforcing the new marijuana law 10% for the Justice Reinvestment Fund |

| California | Weight-based $9.65 per ounce for flowers $2.87 per ounce for leaves $1.35 per ounce for fresh plants 15% state tax on retail purchases 7.25% for state general sales tax Local governments can determine their percentage-of-price and general local sales tax. | Costs of marijuana legalization Programs that address negative impact of drug use, economic development, academic studies and youth programs |

| Colorado | Percentage-of-price 15% for wholesale transactions 15% for retail transactions Local governments can also levy a general local sales tax. | Education programs |

| Connecticut* | Potency-based 0.625 cents per milligram for plants 2.75 cents per milligram for edibles 0.9 cents per milligram for other products Percentage-of-price 6.35% state general sales tax 3% for local governments | Social equity programs Drug-prevention and recovery programs |

| Illinois | Potency-based 10% of the retail price when THC content is 35% or less 25% of the retail price when THC content is 36% or higher All marijuana-infused products are taxed at 20% of the retail price. | Costs associated with marijuana legalization Remaining revenue: State general fund Substance abuse programs Local government transfers Criminal justice reform programs |

| Maine | Weight-based $335 per pound for flowers or mature plants $94 per pound for trim $1.50 per immature plant or seeding $0.35 per marijuana seed 10% excise tax on retail sales price | 50% for public health and safety programs 50% for law enforcement training programs related to the legalization of marijuana |

| Maryland | Not Yet Determined | Development of the Cannabis Public Health Advisory Council and the creation of the Cannabis Public Health Fund |

| Massachusetts | Percentage-of-price 10.75% for retail transactions 6.25% for state general sales tax on purchases 3% for local sales tax on purchases | Various public safety programs |

| Michigan | Percentage-of-price 10% tax for retail transactions 6% state general sales tax | Education, Transportation Transfers to local government |

| Montana | Percentage-of-price 20% tax for retail transaction Localities can levy 3% for retail sales purchases | Environmental conservation Substance abuse prevention and treatment Veterans’ services Health careLocal government Resentencing efforts for people previously convicted for |

| Nevada | Percentage-of-price 15% for wholesale transactions 10% for retail transactions 6.85% for state general sales tax Localities can levy a sales tax on all retail purchases. | Education programs State’s rainy-day fund |

| New Jersey* | Weight-based 33% for retail price per ounce for the first nine months After the first nine months: $10 per ounce if the retail sale is $350 or more $30 per ounce if the retail sale is between $250 and $349 $40 per ounce if the retail sale is between $200 and $249 $60 per ounce if the retail sale is less than $199 Percentage-of-price 6.625% for state general sales tax on purchases Localities can levy up to 2% local sales tax on purchases | 70% for Impact Zones (i.e., neighborhoods affected by prior marijuana laws) 30% for administrative costs for legalization and for the state general fund |

| New Mexico* | Percentage-of-price 12% for retail transactions until July 2025 Each year the tax will rise 1% until it reaches 18% in 2030. State and local sales taxes may also be implemented. | Administration of marijuana statutes, Localities where the sales transactions occur and Deposit to state general fund |

| New York* | Percentage-of-price 9% state level excise tax 4% local level excise tax Potency-based 0.5 cents per milligram of THC for flower 0.8 cents per milligram of THC for concentrates 3 cents per milligram of THC for edibles | School districts Drug treatment Public Education Reinvestment grants for community-based organizations Administrative and research costs for marijuana usage studies |

| Oregon | Percentage-of-price 17% for retail transactions Additionally, localities can levy up to 3% of the retail price | Education programs, Drug prevention and treatment programs Transfers to local governments |

| Rhode Island | Percentage-of-price 7% state general sales tax 10% new cannabis tax 3% municipality tax, wherever marijuana is sold | Public health and public safety |

| Vermont* | Percentage-of-price 14% for retail transactions 6% for state general sales tax Local governments can levy a sales tax. | After-school learning programs |

| Virginia* | Percentage-of-price 21% for retail transactions 3% for local excise tax 5.3% state general sales tax Local governments can levy a sales tax | Pre-kindergarten programs Reinvestment grants for underserved communities Drug prevention and treatment programs |

| Washington | Percentage-of-price 37% for retail transactions 6.5% for general state sales tax Local governments can levy a local sales tax | Health care programs |

For more information on marijuana taxes, please visit The Book of States, produced annually by The Council of State Governments: https://issuu.com/csg.publications/docs/bos_2021_issuu